GMX Treasury — Three-Fund Architecture, esGMX-Only Discounts (up to −80%), and 50/50 Fee Distribution

(TL;DR)

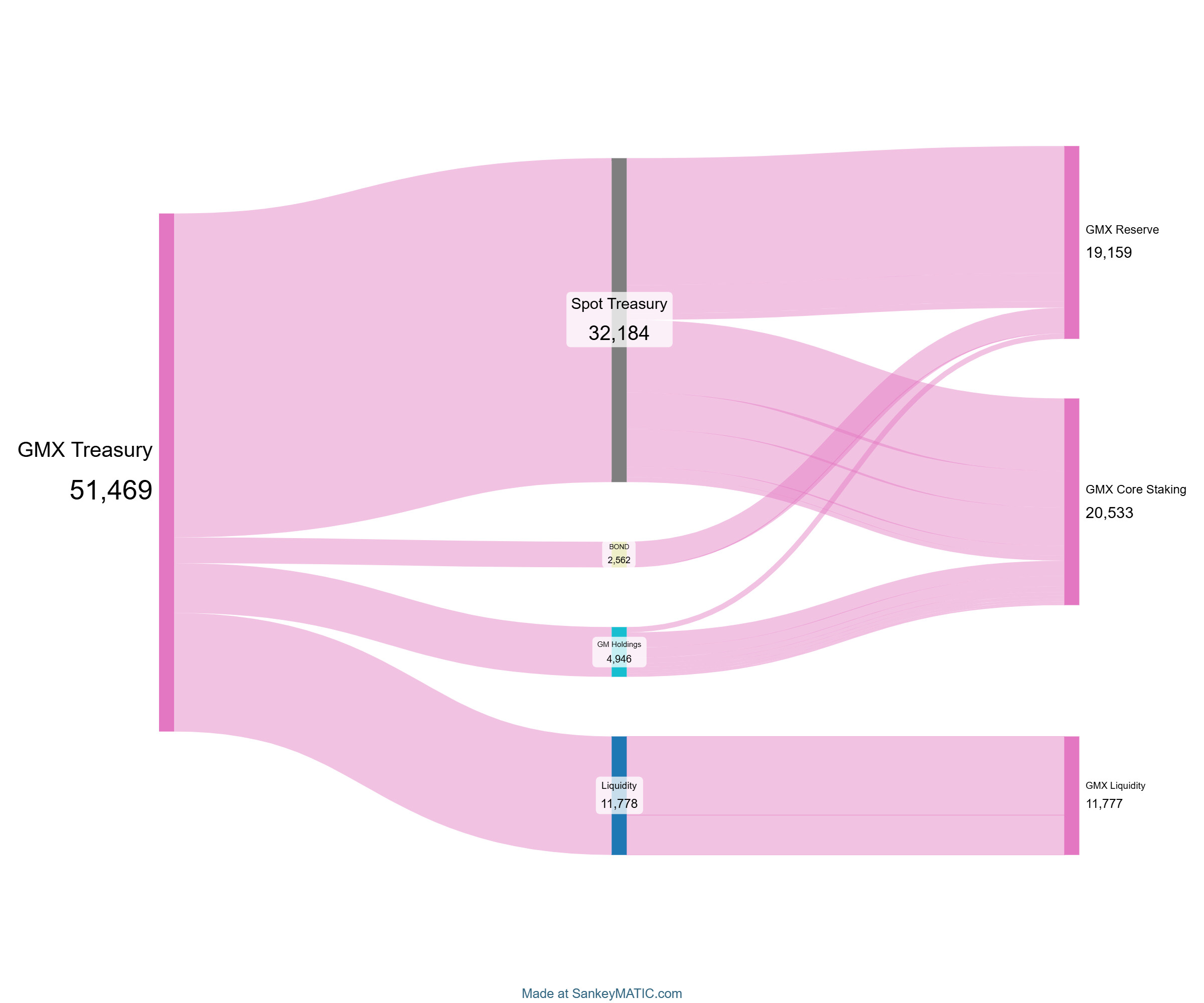

Split the Treasury into three funds with clear routing:

GMX Reserve — maintain a GMX:esGMX target mix (default 50:50) to fund incentives.

GMX Core Staking — earn conservative yield on ETH/BTC/SOL/AVAX (plus GLV/GM pools); reallocate ≤20% NAV/year to buy GMX for the Reserve; sources include Uniswap ETH fees and 10% of GMX v2 fees.

GMX Liquidity Incentives — run incentive programs with a GMX+esGMX budget (default 50:50) and manage Uniswap v3 LP NFTs (which already earn swap fees). Consider moving selected 1.0% fee-tier pools to 0.3% where it improves execution/fee capture.

esGMX-only trading fee discounts with a cap of −80% versus GMX v2 base fees.

Staker distributions switch to 50% esGMX + 50% GMX (instead of 100% GMX).

Mandate

Operate incentive programs and LP positions to grow liquidity, volume, and OI:

Uniswap v3 LP NFTs (already live; no structural change). Operational note: evaluate migrating selected 1.0% fee-tier pools → 0.3% . Most major protocols (e.g., Aave, LINK, ENA) concentrate liquidity primarily in 0.3% fee-tier pools.

Incentive budget in GMX + esGMX (default 50:50) for trading campaigns, OI growth, and support for key pools (including upcoming tokenized-asset pools such as gold/stock-linked).

Principle

Only accounts that hold/lock esGMX qualify for trading fee discounts applied to GMX v2 base fees; maker and taker discounts are each capped at −80%.

i think using the treasury to buy GMX and distribute for incentives makes sense

i feel it may be preferable to use GMX instead of esGMX to reduce the dev time needed, because esGMX introduces some complexities e.g. the vestable esGMX amount needs to be updated on claim, and this adds complexities for integrations as well

fee discounts makes sense, i think it should be GMX based though, otherwise it would be difficult for new users to access the fee discount

staking ETH in Lido or AVAX in Benqi i think is fine

i think we should be careful with allocating too much of the treasury to GLV / GM pools or any other yield generating avenues though, because the treasury is also necessary to back the Immunefi bounty and as a last resort for LP reimbursements, because exploits are so common my opinion is being extra cautious here is necessary

to clarify, we should still allocate a portion, i just mean that we should not allocate the entire treasury, and ensure that a sufficient amount is kept for bounties, etc

i also have no objections to using a portion of the treasury for incentives to grow the protocol

Actually I like “Proposal 3” a lot. After MP abandoning GMX price is suffering (as I predicted) because there no obstacles left for unstacking and selling it whenever you want. We need some barriers to promote GMX staking stickiness. Distributing part of rewards as esGMX will do the job. Main advantages:

Immediate effect - less selling pressure just after rewards claim, because esGMX should be vested first and it takes 1 year to fully vest it;

Locks staked GMX as reserve for esGMX vesting. While vesting you can’t freely unstake and sell GMX because it is locked. Only way to unlock is by abandoning vesting and withdrawing esGMX from vesting vault. But it is unfavorable because next time you need to restart vesting from beginning. Lets say someone is vesting 5000 esGMX for 1 year already and still has 1000 esGMX left to unvest. By doing nothing it will take 1/5 year to finish vesting these 1000 esGMX. But if you abandon vesting and restart fresh later it will take another full 1 year to unvest remaining 1000 esGMX. So it worth considering before GMX unreserve/unstake/sell;

Because of final GMX bag unstaking/selling some esGMX from rewards will never be converted to GMX so it is even bigger reduction in long term sell pressure;

Better APR to long term stakers - vested esGMX don’t get rewards, so loyal stakers who stake all their GMX/esGMX without vesting will get a bit larger rewards share;

And another important advantage of this proposal is it’s easy implementation - all contracts for esGMX distribution and vesting already developed/audited/deployed and time tested. Because we had esGMX rewards in the past and UI still has sections mentioning esGMX. Only burden for devs is to change a bit workflow of weekly bought back GMX distribution- cutting it in half and minting appropriate amount of esGMX for distribution thru old distribution contract.

Thank you X for the thoughtful feedback.

After reviewing Hyperliquid’s fee/VIP design and the GMX Referral Program analytics (see: https://dune.com/adamzjw/gmx-referral-program), it’s clear that recent trading volume should be a first-class input for fee tiers. Given GMX’s current weekly volume (~$1.5–2.5B over the last 2–3 months), the rollout plan for Proposal 2 is below.

Example A (mid-tier): VIP2 (−35%) + GMX Booster D (−30%) + Referral Tier 2 (−10%), Base = 0.06%

→ 0.06 × 0.65 × 0.70 × 0.90 = 0.02457% (≈ 2.457 bps)

Example B (top-tier clamps): VIP5 (−80%) + Booster E (−40%) + Referral (−10%), Base = 0.06%

→ exceeds the 80% cap → clamped at 0.012%; if Base = 0.04%, clamp at 0.008%; then apply the 1 bp floor if needed.

“In Proposal 1 — Three-Fund Architecture, I’m focused on the Treasury’s structure and the roles of each fund. Once Proposal 1 is approved, I believe we’ll need further discussion to develop a complete implementation plan.”